What are the reasons for the "interest rate cut tide" set off by "CCB Viewpoint" banks? Where is it going?

At the beginning of September, 2023, the third round of interest rate reduction of bank deposits began against the background of the downward yield of 10-year treasury bonds and the downward adjustment of one-year LPR quotation. The downward interest rate of bank deposits will help ease the pressure of narrowing the bank’s net interest margin and enhance the bank’s ability to resist financial risks; At the same time, guide the transformation of deposits into consumption and investment, and bring incremental funds to the market. However, depositors set off a "craze for opening accounts in Hong Kong", and the willingness to de-leverage was high in stages, which weakened the effectiveness of the deposit interest rate reduction policy. There is still room for relaxation of China’s monetary policy, and the average cost ratio of corporate demand deposits remains high, which makes it difficult for commercial banks to reduce the deposit interest rate and reduce costs. It is expected that there will still be room for further reduction of the deposit interest rate in the fourth quarter, but the reduction is limited.

01

Under the guidance of six major state-owned banks,

Major banks have entered a "wave of interest rate cuts"

Since the second half of 2022, under the leadership of state-owned banks, bank deposit interest rates have experienced three rounds of downward adjustment:

First, on September 15, 2022, six major state-owned banks collectively adjusted the interest rates of various varieties, involving time deposits and demand deposits. Among them, deposit interest rate lowered the three-year lump-sum deposit and withdrawal interest rate by 5 basis points, lowered the three-year lump-sum deposit and withdrawal interest rate by 15 basis points to 2.6%, and lowered the remaining term by 10 basis points. Subsequently, joint-stock banks and city commercial banks followed suit. After experiencing the economic downturn in the first half of 2022, the monetary policy in the second half of the year focused on expanding investment and promoting consumption, focusing on the supporting role of the banking industry as a financial entity to the economy. The monetary policy tends to be loose, but the policy is still being explored. Compared with the deposit interest rate reduction cycle in 2023, this round of adjustment is relatively soft.

Second, on June 8, 2023, in order to adapt to the new market situation, the six major banks adjusted their regular and deposit interest rate again. Among them, deposit interest rate reduced by 5 basis points to 0.2%, and the adjustment range was relatively small; The interest rates of two-year, three-year and five-year fixed deposits were lowered by 10 basis points, 15 basis points and 15 basis points respectively, and the adjusted interest rates were 2.05%, 2.45% and 2.5% respectively, which was larger than that in September 2022. Subsequently, joint-stock banks and city commercial banks successively followed suit. In the first half of 2023, China’s macro-economy entered an upward channel of repair, but the overall situation was still less than expected.

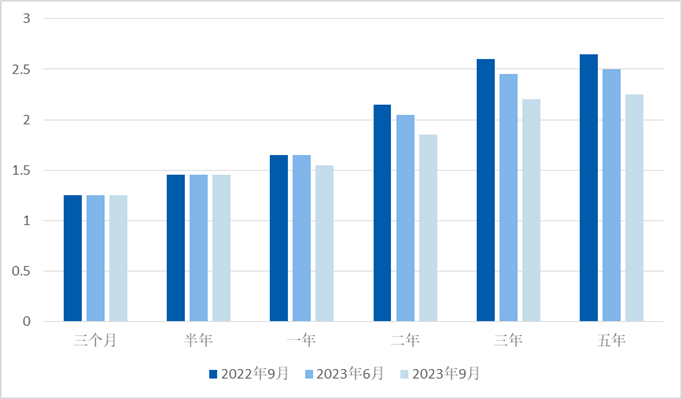

Third, in order to lay a solid foundation for the recovery in the first half of the year, guide the flow of funds to the real economy, reduce the cost of social financing, and at the same time ease the operating pressure caused by the narrowing of net interest margin, the banking industry further lowered the deposit interest rate. At the beginning of September, 2023, faced with the new business situation, the third round of bank deposit interest rate reduction kicked off. Six major state-owned banks took the lead in announcing the reduction of deposit interest rate, and joint-stock banks and city commercial banks followed suit. The adjustment range is between 10 and 25 basis points, and the banks are divided, and the decline rate is further increased compared with the previous two interest rate reductions. Take ICBC as an example. After three rounds of adjustment, the interest rates of three-month, six-month, one-year, two-year, three-year and five-year time deposits are 1.25%, 1.45%, 1.55%, 1.85%, 2.2% and 2.25% respectively.

Figure 1: Changes of deposit interest rate of ICBC from 2022 M9 to 2023 M9.

(Unit:%)

02

Banks set off a wave of interest rate cuts.

What is the reason?

This has to start with the reference index of China’s deposit interest rate. The change of deposit interest rate in China mainly refers to the change of bond market interest rate and loan market interest rate, which are based on the yield of 10-year government bonds and the quotation of 1-year LPR respectively.

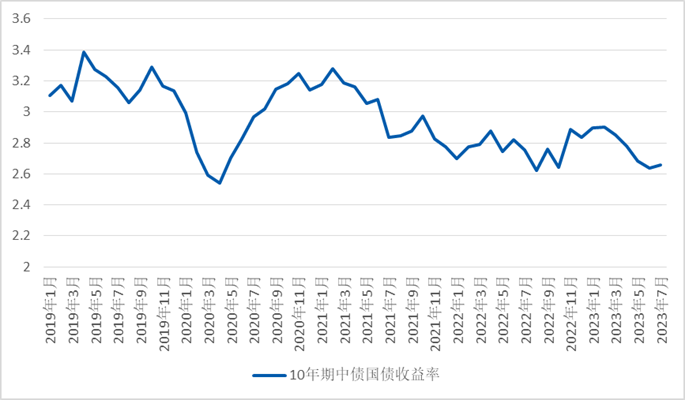

In terms of the yield of national debt, since 2021, due to the slowdown of economic growth and the interest rate cut by the central bank, China hasThe yield of 10-year treasury bonds showed a downward trend of volatility.. In July 2021, the yield of China’s 10-year treasury bonds fell below 3%, and it is still hovering at the low level of "2 prefix", leading to a large-scale flow of funds to banks. According to the data of the central bank, in 2022, China’s new RMB deposits were 26.26 trillion yuan, an increase of 6.59 trillion yuan over the same period in 2021, setting a new high in recent years. In order to avoid large-scale capital pouring into bank time deposits, play the role of market-oriented adjustment mechanism of deposit interest rates, stabilize bank debt costs, and promote market investment and consumption, it is imperative to lower bank deposit interest rates.

Figure 2: Yield of China’s 10-year medium-term bonds from 2019 M1 to 2023 M7

(Unit:%)

In terms of LPR, the LPR reform officially landed in 2019, which made China’s interest rate transmission mechanism smoother. The LPR quotation method generated by adding the medium-term lending facility (MLF) interest rate greatly improved the effect of monetary policy. Since 2023,China’s one-year LPR quotation went through two rounds of downward adjustment in June and August respectively.. According to the data of the National Interbank Funding Center authorized by the People’s Bank of China, in June 2023, the interest rates of short-term loans and long-term loans declined, and the 1-year and 5-year LPR decreased by 10 basis points from the previous value to 3.55% and 4.20% respectively; In August, 2023, the one-year LPR was lowered by 10 basis points to 3.45% again, and the LPR over five years remained unchanged. In addition, in September, the interest rate reduction of major banks’ stock mortgages officially landed, and the banking industry generally faced the pressure of narrowing the net interest margin.

In this context, pushing down the interest rate of bank deposits is conducive to reducing the debt cost of banking institutions, maintaining the stable operation of the banking industry, and at the same time pushing down the financing cost of the real economy, further improving the quality and efficiency of banking services to the real economy.The downward trend of the main reference index of bank deposit interest rate is driving the domestic bank deposit interest rate into the deep-water period of elastic change..

03

The wave of bank interest rate cuts "strikes",

Affect geometry?

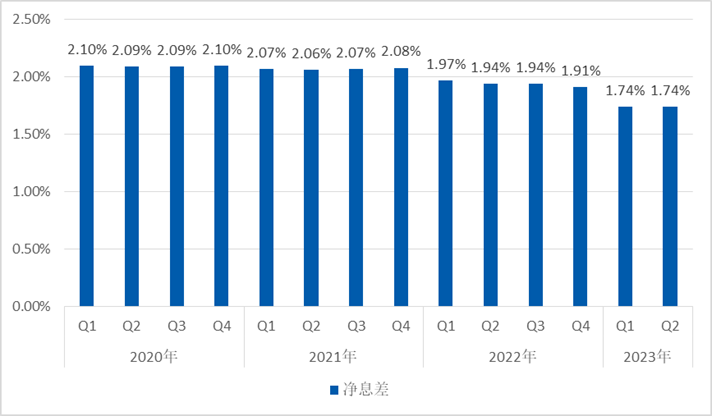

The impact on banksIn recent years, affected by the reduction of LPR for many times and other factors, the interest rate of new loans has decreased, and the return on assets of commercial banks has been under pressure, facing many challenges such as increasing liabilities, increasing the average cost rate of customer deposits and narrowing the net interest margin. In the first half of 2023, the net interest margin of Agricultural Bank, Industrial and Commercial Bank of China, China Construction Bank, Bank of Communications, Postal Savings Bank and China Bank decreased by 36 basis points, 31 basis points, 30 basis points, 22 basis points, 19 basis points and 9 basis points respectively, which were 1.66%, 1.72%, 1.79%, 1.31% and 2.03% respectively. From September 25, 2023, the bank lowered the interest rate of commercial personal housing loans for the first set of housing, and the mortgage interest rate entered a period of parallel downward adjustment of incremental housing and stock housing. The declining financing costs of enterprises and residents further narrowed the net interest margin of banks. The data shows that the net interest margin of China’s banking industry has dropped from 2.08% in Q4 in 2022 to 1.74% in Q2 in 2023. Under the macro-economy disturbed by the external environment, the narrowing of the net interest margin of the banking industry is irreversible, and the profitability of banking institutions is under pressure. The second round of bank deposit interest rate reduction in the year, which started in early September, 2023, is the supporting policy for the interest rate reduction of existing mortgage loans. The decline in asset-side income forced banks to cut deposit interest rates and reduce debt costs. To a certain extent,Relieve the pressure of narrowing the bank’s net interest margin and enhance the bank’s financial risk resistance..

Figure 3: Trend of net interest margin of commercial banks in China from 3:2020Q1-2023Q2.

(Unit:%)

The impact on the economy.China’s macroeconomic fundamentals still need to be repaired by lowering interest rates, and the low inflation environment provides a favorable environment for loose monetary policy. The reduction of deposit interest rate is expected to stimulate residents’ consumption in disguise, while the double reduction of loan interest rates for incremental houses and stock houses will drive the marginal recovery of real estate sales. The effect of combine monetary policy is released,It will guide the transformation of deposits into consumption and investment, bring incremental funds to the market, and promote a virtuous circle of economy and finance.To ensure that the macro economy operates within a reasonable range.

Depositors set off a "craze for opening accounts in Hong Kong", and their willingness to deleverage was high in stages, which weakened the effectiveness of the policy of lowering deposit interest rates.. While the interest rate of deposits in the Mainland is falling, the interest rate of deposits in Hong Kong is rising. With the widening spread between Hong Kong and the Mainland, the attractiveness of mainland banking institutions in China to depositors has weakened, and depositors have sought alternatives one after another, setting off a round of "opening accounts in Hong Kong". According to the data of the Hong Kong Monetary Authority, in August 2023, the total deposits of authorized institutions in Hong Kong increased by 0.6% month-on-month, of which Hong Kong dollar deposits, foreign currency deposits and RMB deposits increased by 0.4%, 0.8% and 6% respectively, and RMB deposits increased significantly faster than other currency types, which weakened the effectiveness of the deposit interest rate reduction policy to some extent. In addition, although the policy starting point of lowering the deposit interest rate is to reduce the cost of bank debt and boost consumption, it also impacts the residents’ willingness to increase leverage and consumption to some extent. On the one hand, affected by interest rate changes, residents’ willingness to repay loans in advance with deposits is on the high side; On the other hand, residents expect more uncertainty in the future, have a strong precautionary saving mood, and tend to reduce consumption to cope with the possible economic cold wave. How to guide the effective transfer of funds to the real economy has become a new topic facing China’s financial industry.

04

Banks cut deposit interest rates one after another,

Where is it going?

On the whole, western countries are tired of coping with the persistently high inflation rate and the Palestinian-Israeli conflict. The global macroeconomic situation is still unclear, and China’s monetary policy still has some room for relaxation. In addition, the average cost rate of enterprise demand deposits remains high, which makes the commercial banks’ lowering the deposit interest rate and reducing costs not achieve the ideal effect yet.It is estimated that there is still room for further reduction of deposit interest rate in the fourth quarter, but the reduction is limited.. On the one hand, the stable operation of macro-economy still needs the combination of monetary policy; On the other hand, the banking industry not only has fierce internal competition, but also faces the squeeze from financial institutions such as public offering, brokerage and insurance. Further lowering the interest rate of bank deposits will weaken the attractiveness of banks to funds. While lowering the deposit interest rate, it is very important for the supervision to give full play to the joint efforts of monetary policy and push the macro-economy into a rapid repair channel to avoid continuously impacting the investment of enterprises and the consumer confidence of residents, so as to build a positive economic cycle mechanism.

Contributed by: Wang Xinya, Investment Consulting Department of Headquarters

Editor: Sun Wenxin

Planning: Headquarters Office

[Important Statement]